Understanding DAC8

What is DAC8?

DAC8 is Directive (EU) 2023/2226, the EU crypto-asset tax reporting directive that extends automatic exchange of information to crypto transactions.

Updated

Short answer

DAC8 is Directive (EU) 2023/2226, adopted on 17 October 2023. It is the eighth amendment to the European Union’s Directive on Administrative Cooperation in taxation (Directive 2011/16/EU). It extends automatic exchange of information between EU tax authorities to reportable crypto-asset transactions.

Starting in 2026, reporting crypto-asset service providers must collect and report information about reportable users and transactions. Tax authorities can then exchange that information automatically.

DAC8 does not create a new EU crypto tax. It creates a reporting and data-exchange infrastructure that helps tax authorities enforce existing national tax rules. In practice, DAC8 is the European version of the OECD CARF logic: crypto-asset service providers become tax-data collectors, and the data then circulates between administrations.

Visual summary

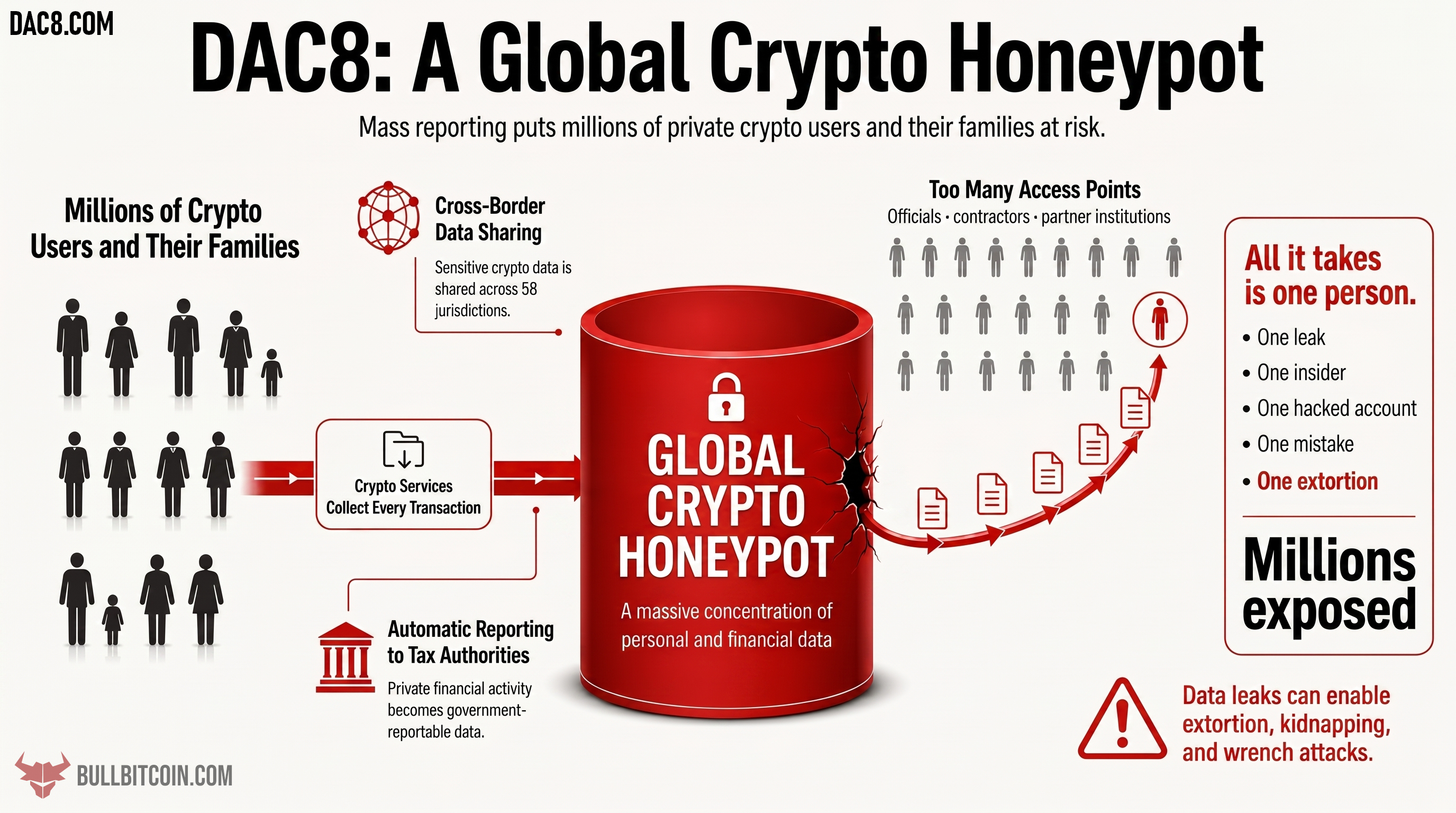

Open the image to inspect the full DAC8 reporting flow. The infographic is a visual aid; the legal details below remain anchored in Directive (EU) 2023/2226 and the European Commission DAC8 documentation.

Key facts

| Question | Answer |

|---|---|

| Formal name | Council Directive (EU) 2023/2226 |

| Also known as | DAC8, the eighth amendment to Directive 2011/16/EU |

| Adopted | 17 October 2023 |

| Published | 24 October 2023 (Official Journal) |

| Entered into force | November 2023 |

| Transposition deadline | 31 December 2025 |

| Application date | 1 January 2026 |

| First reporting period | 2026 calendar year |

| First exchanges | 2027 |

| Main subject | Automatic reporting and exchange of crypto-asset information |

| Global counterpart | OECD Crypto-Asset Reporting Framework, or CARF |

| Scope reference | MiCA, Regulation (EU) 2023/1114 |

DAC8 and CARF

DAC8 is closely aligned with the OECD Crypto-Asset Reporting Framework. CARF is the global standard; DAC8 is the European Union legal instrument that applies a similar reporting logic inside the EU.

Both frameworks pursue the same official objective: giving tax authorities systematic visibility over crypto transactions carried out through service providers.

Background

The Directive on Administrative Cooperation created a framework for exchanging tax information between Member States. Successive DAC versions extended that framework to new categories of information.

DAC8 adds crypto-assets to this architecture. The official rationale is that a visibility gap existed between traditional finance, already covered by automatic-exchange regimes, and crypto markets, where the older concepts of financial account or financial institution did not always cover service providers.

Which assets are in scope?

DAC8 relies on concepts close to MiCA. The scope can include cryptocurrencies, stablecoins, certain tokenized assets and certain NFTs when they are used for payment or investment purposes.

The important point is that the scope is not limited to Bitcoin or to a single category of tokens. It broadly targets crypto-assets that can be transferred, exchanged or used as economic value.

Who is affected?

The reporting burden falls on reporting crypto-asset service providers. In practical terms, this can include exchanges, brokers, custodians, trading platforms, payment services and other providers that effectuate or facilitate reportable crypto transactions.

Users are affected when they are reportable users under the applicable rules. A user can be reportable because of tax residence, entity status, controlling-person rules or activity through a covered provider, in particular when they are tax residents of a Member State.

What data is reported?

DAC8 can cover identity (name, home address, date of birth), tax residence, tax identification numbers, transaction types, values, dates and transfer information, including operations with no tax relevance.

Which transactions are covered?

DAC8 can cover several categories of transactions:

- acquisitions or disposals against fiat currency;

- exchanges between crypto-assets;

- transfers of crypto-assets;

- certain retail payments;

- values, volumes and units per type of crypto-asset.

These categories show that DAC8 is not only capital-gains reporting. The mechanism can cover flows and transfers that do not necessarily have the same tax status in each Member State.

Due diligence and reporting

Providers must identify reportable users, determine their tax residence, collect the necessary tax information and produce an annual report to the competent authority.

The authority can then exchange that information automatically with the relevant tax authorities.

Why crypto reporting is different

Crypto reporting is not just ordinary account reporting with a new asset class. A public wallet address can expose a transaction graph. Once that address is linked to a civil identity, observers may infer holdings, counterparties, past activity and sometimes future movements.

That is why the security question is different from traditional bank-account reporting. A leaked bank account number is sensitive. A leaked identity-linked wallet address can become a map of public blockchain activity.

Timeline

- 17 October 2023: DAC8 was adopted by the Council of the European Union.

- 24 October 2023: DAC8 was published in the Official Journal.

- November 2023: DAC8 entered into force.

- 31 December 2025: Member States had to transpose the directive into national law.

- 1 January 2026: Core crypto reporting rules apply, and the first information concerns the 2026 calendar year.

- 2027: First reporting and automatic exchange cycle for 2026 data.

What DAC8 does not do

DAC8 does not harmonize the taxation of crypto-assets across the European Union. Capital gains, income, staking, professional activity and wealth-tax rules remain matters of national tax law.

DAC8 is about third-party reporting. It gives tax authorities external information that can be compared with taxpayer filings.

Impact for crypto businesses

Crypto businesses must build or adapt compliance systems: user classification, self-certifications, transaction aggregation, reporting formats, data retention and client communication.

This burden mechanically favors the largest and best-capitalized players. Smaller providers may be pushed to reduce their offering, consolidate or leave certain markets.

Impact for users

Users who are tax residents of the European Union should expect their reportable activity through covered providers to become visible to the tax authority.

They remain responsible for their own tax filings, but the authority now receives third-party data. The problem is that this data is not only fiscal: in the crypto case, it can also reveal personal security information.

Why Bull Bitcoin opposes DAC8

Bull Bitcoin does not oppose the principle of crypto taxation. The problem is automatic mass collection: it links civil identity, home address, crypto activity and value signals, centralized and shared between tax administrations.

In crypto-assets, this combination can create a physical risk. A leak or abusive access can help target holders and their families.

Bull Bitcoin’s position is that tax authorities already have targeted tools, including information requests directed at identified taxpayers or specific investigations. In France, this targeted power is known as the “droit de communication”. The issue is proportionality: targeted cooperation is different from routine mass collection and cross-border dissemination of sensitive crypto data.

Related pages

- What is CARF?

- DAC8 vs CARF

- CARF reporting requirements

- What data does DAC8 collect?

- DAC8 reporting requirements

- DAC8 reporting deadlines

- DAC8 scope: assets, providers and users

- Impact for crypto businesses

- Impact for crypto users

- History of the DAC directive

- DAC8, MiCA and DORA

- Targeted information requests

- DAC8 and CARF glossary